BIZCHINA> Review & Analysis

|

BIZCHINA> Review & Analysis

|

|

China's auto industry races toward spring

By Sun Dajun (chinadaily.com.cn)

Updated: 2009-06-04 10:17

A mid- and long-term projection and analysis of the 2009 Chinese passenger car market China's auto industry, after several years of rapid growth, faced a turning point in 2008, sliding into a bleak winter. Just as Liu Chuanzhi, one of the founders of Lenovo, said, it is unclear whether it is the winter of Harbin, Beijing or even the Arctic.

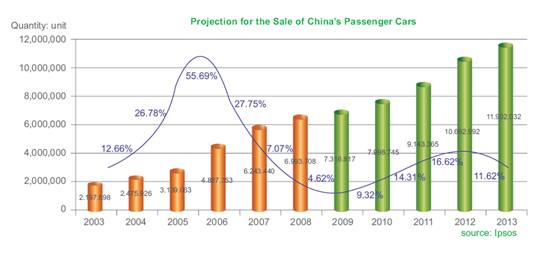

The year 2011 will see a new wave of rapid growth Using a plethora of resources, Ipsos builds a demand model of China's auto market to predict car sales and give auto enterprises an insight into the future market. The above graph is concluded based on this model. The potential variables of this model include four factors that affect the auto market, namely, the macroeconomic performance, purchasing power, energy and raw materials, and transportation infrastructure. Varying amounts of observed variables are assigned to each potential variable as indexes. The fluctuation and decline of the auto industry in 2008 was largely due to the macro regulation and the international economic volatility, which resulted in the capital shortage of auto enterprises. Potential car buyers' concerns about the future and the expected rapid income decline persuaded them to put off or even give up their car purchasing plan. Ipsos believes these adverse impacts are being gradually eliminated. First, the impact of the ongoing financial crisis on China's real economy is limited, leaving the export industry hardest hit. Since the export business of China's auto industry started relatively late and accounts for a small part the auto industry's profit, the auto industry is affected very little by the global crisis. Second, the plan for revitalizing the auto industry, launched by the Chinese government, covers more than ten areas, including policy incentives for new energy cars, subsidized car purchasing in the rural areas, "old-car-for-new-car" scheme, government car procurement, merger and restructuring as well as car loans. The attention paid to the auto industry, shown by the government's rational policy guidance, will effectively stimulate auto consumption. Taking all these factors into account, starting in 2010, China's passenger car market will see a new round of rapid growth, although it is unlikely to reach the same levels witnessed from 2005 to 2007. As the global economy slowly recovers, China's GDP is expected grow at an average annual rate of 8 to 9 percent. The increase in peoples' income will naturally increase demand for cars. Independent innovation, a recipe for staging a comeback In retrospect, great changes were born out of great difficulties. Some people are eliminated in adversity, while others emerge out of it successful and even stronger. The difference between the two groups of people is whether they could find opportunities for survival in times of crisis and create optimal conditions on which to grow out of it. What are the opportunities for auto enterprises? Ipsos believes that in the short term, policies of the auto industry will focus on independent research and development as well as independent branding. Currently, China lacks independent branding in the auto industry, particularly, passenger cars. If there is no independent branding, there will be no core competitiveness. It is predicted that during the eleventh five-year plan China will encourage auto enterprises to forge a development strategy around independent branding, strengthening research and development, and increasing the market share of independent brands. To this end, specific measures are expected to be introduced, for example, favorable taxation policies and fiscal subsidies, which will benefit companies engaged in independent R&D and branding. In the meantime, this policy will also be conducive to independent R&D of auto parts as well as the integration of auto parts enterprises. One of the major reasons for the finished car industry's lack of independent brands is the lack of independent brands in the auto parts industry. Without research and innovation, it is difficult for the latter to achieve synchronized development with the former. The major auto parts of some joint-ventured finished car factories are imported or made by foreign-funded enterprises in China. Ipsos believes that while encouraging the independent innovation of finished car enterprises during the eleventh five-year plan, China will also give policy support to auto parts enterprises that boast an independent brand, R&D advantage, and scale advantage. The cost of car use becomes the deciding factor in car purchasing After identifying the orientation towards independent R&D and independent branding, the next question facing China's auto industry is on what products to focus its R&D. During the eleventh five-year plan, China will encourage the development of energy-saving products. Auto industry-related consumption policies are expected to be introduced. Safety, oil saving, and environmental friendliness will guide the R&D of auto enterprises and the consumption of car users. On the supply side, car manufacturers should shift their strategy during the eleventh five-year plan towards R&D in low-emission and energy saving automobiles. For example, Shanghai Automotive Industry Corporation Group says it will develop microcars and do R&D in hybrid power cars. On the demand side, policies like the consumption tax and fuel tax will be adopted to encourage the purchase of low-emission cars. With the maturing of consumption psychology, car consumption will be more rational, and the cost of car use will become one of the deciding factors in car purchases. Fuel tax is only one of the major costs of car use. Parking fees, traffic conditions and other factors will also have direct and noticeable impacts. At the same time, to save energy, China will phase in the use of diesel in automobiles. For instance, Dongfeng Cummins specializes in middle and heavy-duty truck engines. The Quanshun light buses of Jiangling Motors are equipped with diesel engines. These companies will benefit from the campaign to phase in the use of diesel. The author is research director of Ipsos Auto (For more biz stories, please visit Industries)

|

|||||

主站蜘蛛池模板: 铜山县| 金华市| 额济纳旗| 张家界市| 崇信县| 二连浩特市| 灯塔市| 锡林浩特市| 桐梓县| 罗平县| 图片| 舟山市| 绿春县| 清苑县| 秭归县| 剑阁县| 中西区| 商南县| 金昌市| 五峰| 眉山市| 麻城市| 东乌珠穆沁旗| 武平县| 桓仁| 依安县| 长沙市| 清镇市| 东方市| 潞城市| 诏安县| 阳高县| 疏附县| 清苑县| 西充县| 阿巴嘎旗| 兰州市| 稷山县| 岑溪市| 驻马店市| 武冈市| 阜康市| 任丘市| 平凉市| 仙游县| 依兰县| 谢通门县| 新和县| 昭觉县| 乐清市| 华坪县| 外汇| 海阳市| 香格里拉县| 广安市| 丘北县| 和龙市| 涟源市| 衡阳县| 建阳市| 东乡县| 邵东县| 云浮市| 上林县| 北票市| 察雅县| 浮梁县| 额尔古纳市| 阜南县| 五指山市| 淮南市| 错那县| 布尔津县| 长春市| 芦溪县| 库车县| 陇南市| 临城县| 五河县| 长子县| 临漳县| 兴隆县|